The Framework: Five Rules That Fired This Week, And Why I Built The System That Runs Them

Thirty years of index investing built the working capital. The framework runs the sleeve.

This week the rules said trim two, hold one, watch one, and build into Williams. The trade tickets are in the article.

For most of my working life, I was an index investor. That is not a confession. That is the truth, and for the situation I was in, it was the right call.

I had little kids. I had a job that ran long hours. I had a house and a mortgage and a life that did not have room for the kind of attention required to invest in individual companies responsibly. The market noise was a wall of static and I had no methodology for separating signal from noise. So I did what every honest financial planner tells you to do when the alternative is making it up as you go. I bought broad-market index funds, dollar-cost averaged into them through every paycheck for decades, and let compounding do the work. It built the working capital. It got me to here. It was the right tool for that job at that time.

What changed is that AI tools got good enough to actually separate signal from noise in real time. Not perfectly. Not even close to perfectly. But well enough that I could finally build a methodology for individual stock investing that did not depend on getting lucky or guessing the macro. So I built one. The Freedom Grid framework is the result. It runs an infrastructure stock sleeve that sits inside a larger portfolio that still has plenty of index exposure, because I am not stupid and I am not 30 years old.

That last part is the most important context for this article. I am closer to retirement than to the start of my career. The game has changed. When I was 30, blowing up the portfolio was painful but not catastrophic, because I had three decades of earnings ahead of me to rebuild. At 60, blowing up is the entire thing. Not blowing up is the number one priority. Everything else, including maximizing returns, sits below that.

The framework is built around that priority. Rules over discretion. Mechanical triggers over feel. Documented frameworks over gut calls. There have been occasions, more than I would like to admit, where if I had overridden the rules and taken on more risk, I would have made more money. That is real. I am not pretending the rules are optimal in every cycle. The rules are optimal for the situation I am actually in, which is a 60-year-old whose biggest risk is no longer underperformance. It is permanent capital impairment.

Today I want to walk you through five of those rules. Not the entire framework. The framework has been built up over years and there is more to it than fits in a Substack article. These five are the rules that fired this week. The convergence of signals was clear, the rules said move, and I moved. The trade tickets executed at yesterday’s open. If you are interested in the rest of the framework, tell me in the comments and I will write it out across future articles. Some of these are obvious. Some of them I learned the hard way. All of them exist because I want to maximize returns on this sleeve without ever letting a single bad week end the larger game.

A note before I start. I do not share dollar position sizes. That is a hard rule in this publication. What I will share is everything else. Sleeve percentages, gain ratios, concentration flags, the actual decision logic, and the fill prices from the trade tickets. If you want to follow along with how a concentrated infrastructure sleeve actually breathes, this is what it looks like from the inside.

The Five Rules That Fired This Week

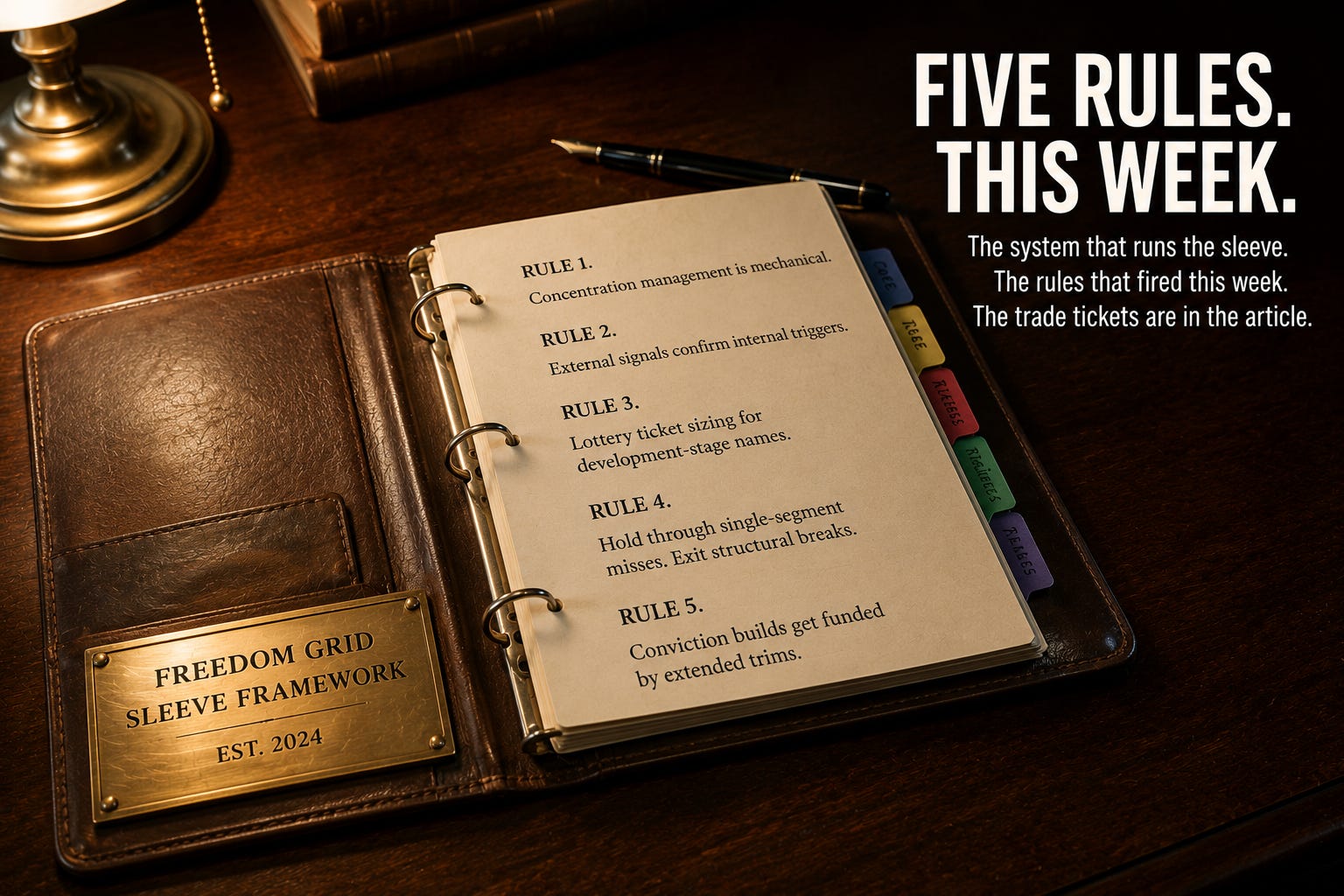

Rule 1: Concentration management is mechanical, not discretionary.

Any single position in the sleeve that hits 10 percent of sleeve weight triggers a YELLOW flag. The rules say take a small chunk off the top, hold the proceeds as sleeve cash, and redeploy where conviction is highest and concentration is lowest. Any position hitting 14 percent of sleeve weight triggers a RED flag, where the trim becomes mandatory rather than optional. The trims are not bets against the company. The trims are bets that no single name should ever be allowed to grow into a position where one bad quarter can take down the entire sleeve. The numbers do not care how much I love the story. This is the rule that exists because every blow-up I read about in financial history happened to somebody who let a winning position get too big and then watched it become a losing position before they could react.

Rule 2: External valuation signals confirm internal concentration signals.

When an independent third-party rule system flags the same names that my internal concentration framework is already flagging, that is the system telling me something I should not ignore. Two rule systems converging on the same names in the same week is signal, not noise. The rules say when the convergence fires, do the work, and do it quickly. Hesitation is what turns a 10 percent trim into a 14 percent forced sale at a worse price.

Rule 3: Lottery ticket sizing for development-stage names.

Companies where the structural confirmation event has not happened yet get a small position size and a defined downside. The position is funded from sleeve cash or house money trims, never from new capital. If the technology delivers, the upside is asymmetric. If it does not, the downside has no allocation impact. The rule prevents the most common portfolio mistake in early-stage infrastructure investing, which is letting a promising development-stage name get sized like a proven business and then taking a permanent capital hit when the proof never arrives.

Rule 4: Full position holds survive single-segment misses, not structural breaks.

When a company in the sleeve takes a bad quarter, the question is not whether to panic-sell or average down. The question is whether the structural reason for owning the company is still intact. If the punishment was for a single segment execution miss inside an otherwise intact franchise, the rule says hold. If the punishment was for a break in the underlying buildout story, the rule says exit. The discipline is in being able to tell the difference under pressure, which is exactly when human judgment is least reliable. The rule exists so I do not have to trust my judgment in the moment.

Rule 5: Conviction builds get funded by extended trims, not new capital.

When a structurally compelling name is sized below its target weight in the sleeve, the rule says build. But the build does not come from raising new capital or stretching position sizes across the rest of the sleeve. The build comes from the cash generated by trimming the names that the rules already said were extended. Extended dollars move down the stack. The sleeve recycles its own profits into its next conviction position. That is the entire engine, and it is why concentration management and conviction building are the same system, not two separate jobs.

Five rules. That is what fired this week. Now let me show you what they produced.

The Convergence That Triggered Everything

On May 11, Seeking Alpha’s quant system published its updated list of industrials stocks carrying an A+ momentum grade. A+ is the highest possible momentum score in their system. Fourteen names made the cut. The wrinkle is that eleven of those fourteen names simultaneously carry an F valuation grade, the lowest possible score. The other three sit at D or D-minus. In plain English, the quant system is telling you these stocks have rallied so hard that their prices have moved well beyond what current fundamentals justify, even as the momentum stays maximally positive.

Five of those fourteen names are in my Freedom Grid sleeve. Bloom Energy. GE Vernova. Powell Industries. Quanta Services. Vertiv. All five carry A+ momentum and F valuation grades as of last week.

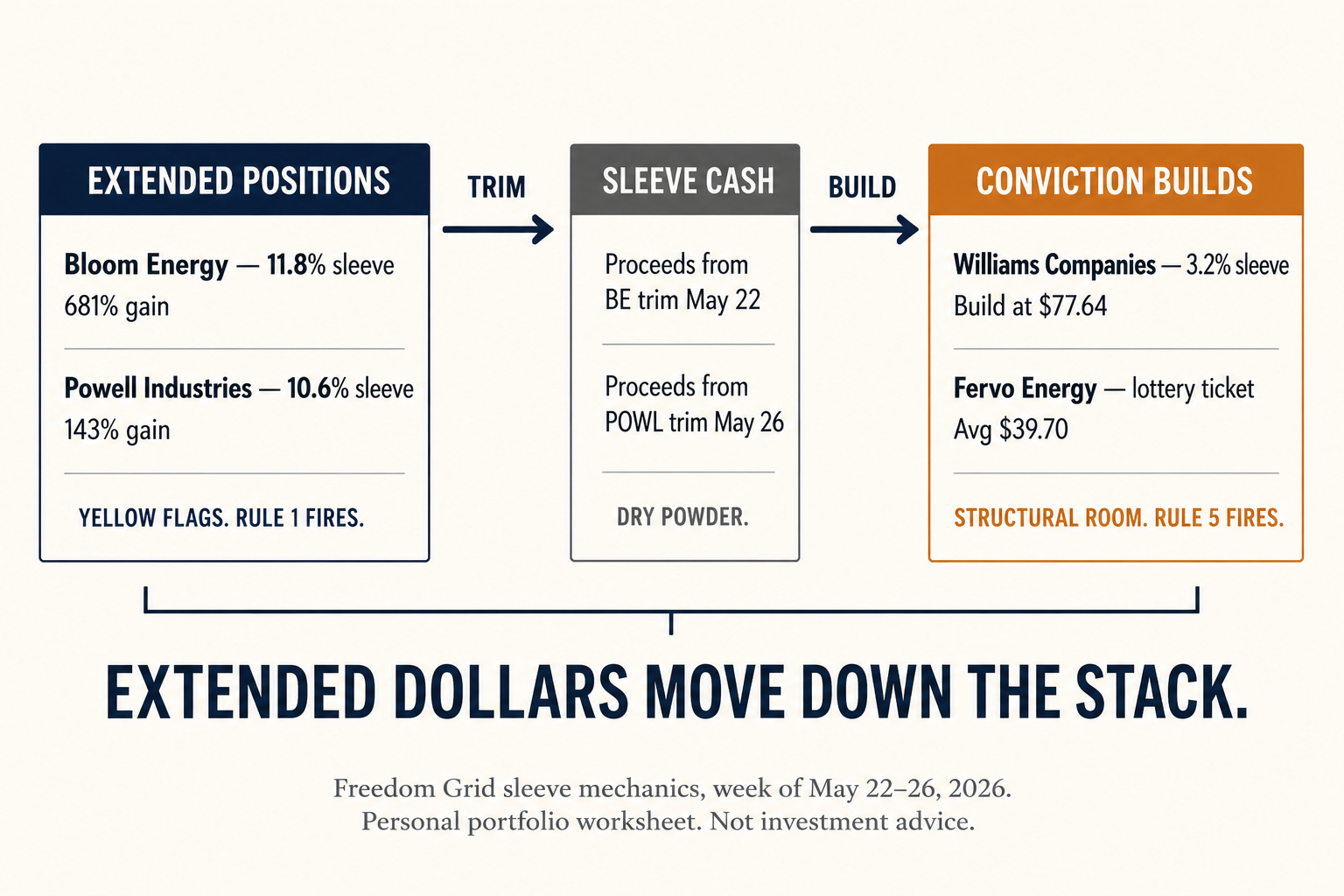

Two of those same five also breached my sleeve concentration YELLOW flag this week. Bloom hit 11.84 percent of sleeve weight. Powell hit 10.65 percent. Rule 1 fires on both. Rule 2 confirms that the internal trigger is not a paranoid one, because an independent quant system is flagging exactly the same names for exactly the same reason. The rules said move. So I moved.

Rule In Action: Concentration Management

Bloom Energy sits at a 681 percent gain on cost basis. Six hundred eighty-one percent. The position is roughly 11.8 percent of the sleeve, fully house money, meaning the original investment has been returned and the entire current value is profit. It carries the YELLOW concentration flag. Powell Industries sits at a 143 percent gain, 10.6 percent of the sleeve, also YELLOW. Vertiv sits at a 128 percent gain, just under 9 percent of the sleeve, currently below YELLOW but rising. Quanta Services sits at an 85 percent gain. GE Vernova sits at a 73 percent gain.

These are not bad companies. They are not broken stories. Bloom is delivering 130 percent revenue growth and just printed its strongest quarter in company history. Vertiv is at the center of the AI cooling architecture buildout. Quanta and Powell are core EPC and electrical equipment names servicing the infrastructure I write about every week. GE Vernova is the gas turbine company every behind-the-meter project needs. These are all real businesses doing real work.

What the rankings are telling you is that the market has priced the next few years of that real work into the share price already. That does not mean the stocks go down tomorrow. Momentum can stay maximally positive for a long time and the F valuation grade does not mean F performance grade. It means if the buildout slows or earnings disappoint, the cushion is thin. The valuation has run ahead of the fundamentals. Howard Marks talks about this constantly. The cycle does not care what the story is. The cycle cares what the price is and what is priced in.

Rule 1 said trim. So I trimmed.

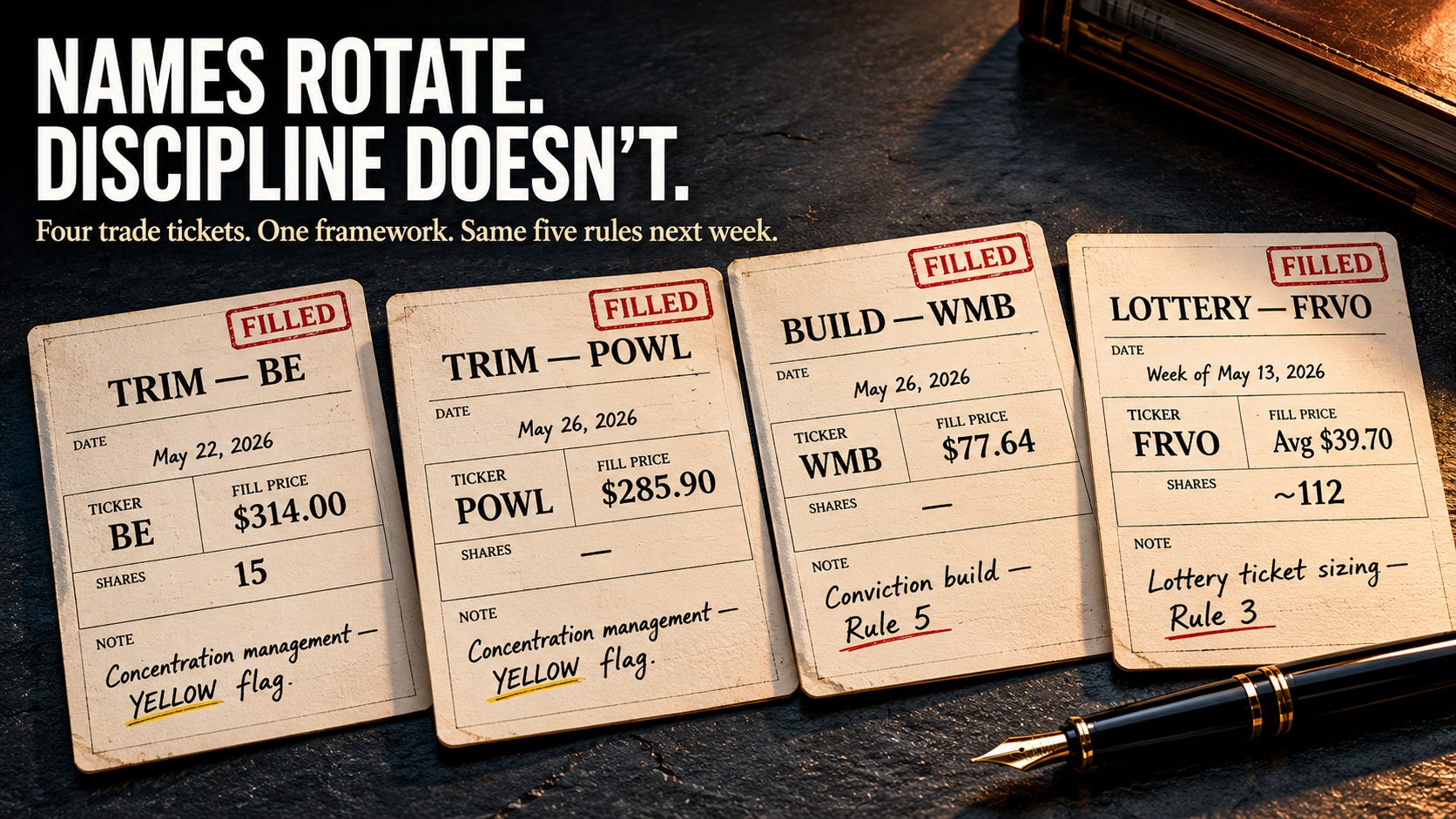

The Bloom trim went in last Friday. 15 shares at $314 on May 22, ahead of the 14 percent RED threshold. Pure concentration management. The proceeds sat in sleeve cash from Friday through Memorial Day weekend and funded part of what executed Tuesday.

The Powell trim went in at Tuesday’s open. Filled at $285.90. Same logic, same rules, same disposition of the proceeds. Both trims are still small relative to the underlying positions. Bloom is still entirely house money. Powell is still a full conviction hold. The concentration came off the top. The structural exposure did not. That is what Rule 1 looks like when it fires correctly.

Rule In Action: Lottery Ticket Sizing

Fervo Energy went public on May 13 as FRVO at $27 and opened at $35. It is the first commercial-scale enhanced geothermal company to hit the public market. Cape Station Phase I is targeted for 100 megawatts of first power in late 2026 and scales to 500 megawatts by 2028. The technology, which uses oil and gas style horizontal drilling and multi-stage fracturing to extract heat from hot dry rock, is real and proven at pilot scale. The bull case is a roughly $7.2 billion contracted revenue backlog and a learning curve from $7,000 per kilowatt today toward a $3,000 per kilowatt nth-of-a-kind target. The financials are tiny. The 2025 revenue was $138,000 against a $58 million net loss. This is a development-stage company that just got priced as a power producer.

Rule 3 says lottery ticket sizing. So that is what I did.

I opened a small position the week of the IPO. Three tranches totaling roughly 112 shares, average cost around $39.70, fully funded from sleeve cash and house money trims from prior positions. No new capital was deployed. The position is small enough that if Fervo never delivers commercial-scale enhanced geothermal on the contracted schedule, the downside has zero meaningful impact on sleeve performance. The position is large enough that if Cape Station fires up on time and the learning curve plays out, the upside compounds without me having to chase later at a higher price.

I am not adding to Fervo until the structural confirmation event arrives. First power at Cape Station is a late 2026 event. The contracted backlog is real but it is paper backlog, not delivered electrons. Until I see commercial-scale enhanced geothermal deliver power to the grid on the contracted schedule, the rules say hold the position where it is.

If you do not own a Fervo lottery ticket yet, Rule 3 still applies. Set a price you are comfortable with as a small position and let the stock come to you. Do not chase. Sizing matters more than entry. The confirmation event is what matters most.

Rule In Action: Full Position Hold Through A Bad Quarter

I am not chasing Primoris because I do not need to. You might.

Primoris reported Q1 2026 on May 5 and the stock got punished. Energy segment execution issues on renewables. 2026 EPS guidance cut from $5.80 to $6.00 down to $4.80 to $5.00. Stock down 28 percent premarket on the print and roughly 40 percent over the following month. As of this writing the stock is trading around $113 to $117.

This is the part where Rule 4 actually earns its place in the framework. Primoris is in my sleeve at a loss and the natural impulse is either to double down to average the cost basis or to sell into the panic to free the capital for something cleaner. Both impulses are wrong. The rule says ask whether the structural reason for owning the company is still intact, and the answer determines whether you hold or whether you exit.

Primoris is the company that builds the gas-fired peakers and the transmission lines and the substations that everybody else’s data center buildouts depend on. They are an EPC business in the cross-phase grid infrastructure segment of the framework. The Utility segment grew in Q1. The Energy segment got hammered on renewables execution. The backlog declined $567 million quarter over quarter but it is still $11.6 billion total including $7.5 billion in master service agreement work. The PayneCrest acquisition closed during the quarter and adds to the long-term EPC footprint. Average analyst price targets sit around $144. DCF fair value estimates run in the $150 range. The Q1 was bad. The franchise is intact.

Rule 4 says hold. So I am holding. I am not adding because I am already at my full position size for this name. I am not trimming because the punishment was for execution on a single segment, not for a structural break in the framework.

If you do not own Primoris and you want exposure to the grid and gas infrastructure buildout, this is a gift. The market priced the company like a structural break when it is actually a single-segment execution miss inside an otherwise intact EPC franchise. The price target consensus implies meaningful upside from here. The risk is another renewables segment surprise on Q2. The reward is paying a 22x trailing multiple for an EPC business that has 60 percent of its backlog under multi-year master service agreements during the largest infrastructure buildout cycle in American history.

Rule In Action: Conviction Build Funded By Extended Trims

That brings us to Rule 5 and the build.

I wrote the full structural case for Williams Companies on Monday. The short version is that Williams quietly transitioned from a pipeline operator to an infrastructure platform company over the last two years. The Power Innovation segment now has six named projects, 2.5 gigawatts of sanctioned capacity, six gigawatts in backlog, and a stated 5x EBITDA build multiple that implies 20 percent project returns. The Transco pipeline business floor still pays the 2.7 percent dividend and is itself growing at 9 percent EBITDA CAGR. The combined business guides to 10 percent or higher adjusted EBITDA CAGR through 2030.

The Bloom Energy rerate from $14 to $310 in twelve months was the market figuring out that solid oxide fuel cells were the speed-to-power solution hyperscalers needed for AI data centers. Williams is the slower-burning version of the same trade, except Williams also owns the gas pipeline feeding every other behind-the-meter project being built by every other company in the eastern United States.

What made Williams the build target Tuesday was Rule 5. Williams sat at roughly 3.2 percent of the sleeve coming into the week. The position had an 8.4 percent gain. There was meaningful room to add before any concentration concern triggered. The setup also lined up with what I was trimming, because the Bloom concentration trim last Friday at $314 and the Powell trim at Tuesday’s open at $285.90 generated exactly the kind of dry powder that Rule 5 wants to deploy into a position with structural conviction and concentration room.

Extended dollars moved down the stack. That is what Rule 5 looks like when it fires.

I bought Williams at Tuesday’s open. Single tranche, market order, filled at $77.64. The trade ticket is what it is. The size was calibrated against the sleeve cash position built from the Bloom trim on Friday and the Powell trim Tuesday. Williams moves from roughly 3.2 percent of sleeve to a higher conviction weight while staying well clear of the YELLOW threshold. That is the build. Done.

I am not adding again this week. The rules say I do not need to. The setup is structural. The catalyst path is eighteen months long. The position is sized to where I want it. The next decision on Williams will be whether to extend the position when the first Power Innovation project hits substantial completion, not whether to chase price action between now and then.

Why I Do Not Override

A short note on something the more aggressive readers are probably thinking. The rules I just walked through are conservative. There are times when overriding them would have made more money. I know this because I have watched it happen in real time. The momentum names I trimmed in prior cycles sometimes ran another 50 percent before pulling back. The conviction builds I sized cautiously sometimes worked spectacularly and I left chips on the table. That is real.

Here is why I do not override anyway.

At 30, the cost of being wrong was time. If I blew up a portfolio at 30, I had three decades of earnings ahead of me to rebuild. The math of compounding was on my side and the recovery window was effectively unlimited.

At 60, the cost of being wrong is permanent. The recovery window is not three decades. It is maybe one decade if I am lucky, and that decade has to fund retirement, not rebuild from scratch. The asymmetry of mistakes has flipped completely. Being right by 50 percent more does not help me if there is a single year in there where I am wrong by 70 percent and never recover. Howard Marks wrote about this his entire career. Nassim Taleb wrote about it in different language. The lesson is the same. Position yourself so that no single bad outcome can take you out of the game.

The rules are the firewall. They are not optimized to maximize the return in any single cycle. They are optimized to ensure that no single cycle ends the game. That is a different objective function than “beat the index every year,” and it produces different decisions. Some of those decisions look like leaving money on the table. They are. The money I am leaving on the table is the insurance premium I pay to never have to start over.

If you are 30, this framework is probably too conservative for you. You have other risks I do not have, and you have time that I do not have. If you are closer to my situation than to 30, then the framework is doing the work it was built to do. Either way, the discipline is the part that transfers. The specific risk tolerance can be tuned to your own situation.

What Else Is In The Framework

The five rules above are not the entire framework. They are the five that fired this week. There are more, and I have built them up over years of doing this work. Some of them are obvious. Some of them I learned the hard way.

If you are interested in the rest of the framework, tell me in the comments. I will write the next layer out across future articles. The things I think about that have not made it into this piece include how I distinguish between a delay in the buildout story and actual damage to the framework, what triggers a name to enter the sleeve in the first place, what triggers an exit, how I think about phase balance across the infrastructure stack, how I manage the lottery ticket basket as a category, what the sleeve cap relative to total portfolio looks like, how earnings season changes the rules, and how I handle macro events that hit the entire sleeve at once. Any of those topics, if there is reader interest, becomes a future article.

The point of writing the framework out in public is not to convince anybody to copy it. The point is that having to articulate the rules forces me to be honest about whether I am actually following them. The accountability is part of the system.

Why The System Is The Product

This is the part where the publication shift I announced earlier this week starts to make sense.

The daily brief was useful but it was very portfolio-specific. It tracked what I was tracking on my timeline. Less useful if you were trying to understand the buildout broadly and develop your own conviction at your own pace. The shift is to deeper company research and sector deep dives, plus articles like this one that show how the work actually gets done, not just what got bought.

The rules are what makes the work repeatable. The rules will still be the rules next quarter and next year. The names will rotate. The sleeve will breathe. Some weeks the rules say do nothing. Some weeks they say trim and build in the same session. The discipline is in following the rules when the moves still feel good as much as when they feel bad.

If you take one thing from this article, take this. The names you see in the headlines are the easy part. The framework that decides which dollar gets the next add and which gets the next trim is where the actual portfolio compounding happens. Most investment writing skips that part because it is harder to write about and easier to fake. I am not skipping it.

Names rotate. The discipline does not.

This Week At A Glance

Bloom Energy, 15 shares trimmed Friday May 22 at $314, concentration management at YELLOW. Powell Industries, trim filled Tuesday May 26 at $285.90, same concentration logic. Williams Companies, single tranche build Tuesday May 26 at $77.64, conviction add funded by the Bloom and Powell trims. Fervo Energy, lottery ticket position opened the week of the IPO at an average around $39.70, no add until Cape Station confirmation. Primoris Services, full position held through the Q1 print, no trim and no add, structural reason for owning the name is intact.

That is the week. The framework will still be the framework next week.

Signal vs. Noise

Signal or Noise: Signal.

The Seeking Alpha A+ momentum / F valuation list is not predictive of near-term price action but it is a useful external confirmation of the same dynamic my internal concentration rules surface independently. When two independent rule systems flag the same names in the same week, the framework says do the work.

The structural buildout we have been tracking, behind-the-meter power for hyperscalers, gas as the only fuel that scales on the right timeline, EPC and grid infrastructure as the throughput constraint, is intact. The names that have run hardest into that story are now extended on valuation. The names that have not yet been priced for it are where the work concentrates from here.

Disclosure

The author holds positions in all the names referenced in this article. This publication does not provide investment advice. The portfolio management framework described is the author’s personal approach and should not be treated as a recommendation for any specific investor’s situation. The framework is built around a specific life stage and risk tolerance and should be tuned to your own situation, not copied directly. Names referenced are analytical examples, not stock recommendations.

Sources

Seeking Alpha, “Caterpillar, GE Vernova, Vertiv: The industrials stocks with A+ momentum and F valuations,” May 11, 2026.

Williams Companies, Q4 2025 earnings release and Investor Analyst Day, February 2026.

Primoris Services Corporation, Q1 2026 earnings release and conference call transcript, May 5-6, 2026.

Fervo Energy, IPO pricing announcement, May 12, 2026.

Bloom Energy, Q1 2026 10-Q and Oracle MSA expansion 8-K, April 2026.

Personal portfolio worksheet, May 22, 2026 snapshot.