Amazon Cut Its Data Center Water. Don’t Believe the Number.

The water didn’t vanish. It moved twenty miles upstream to the power plant, which drinks multiples more, and it landed off Amazon’s books.

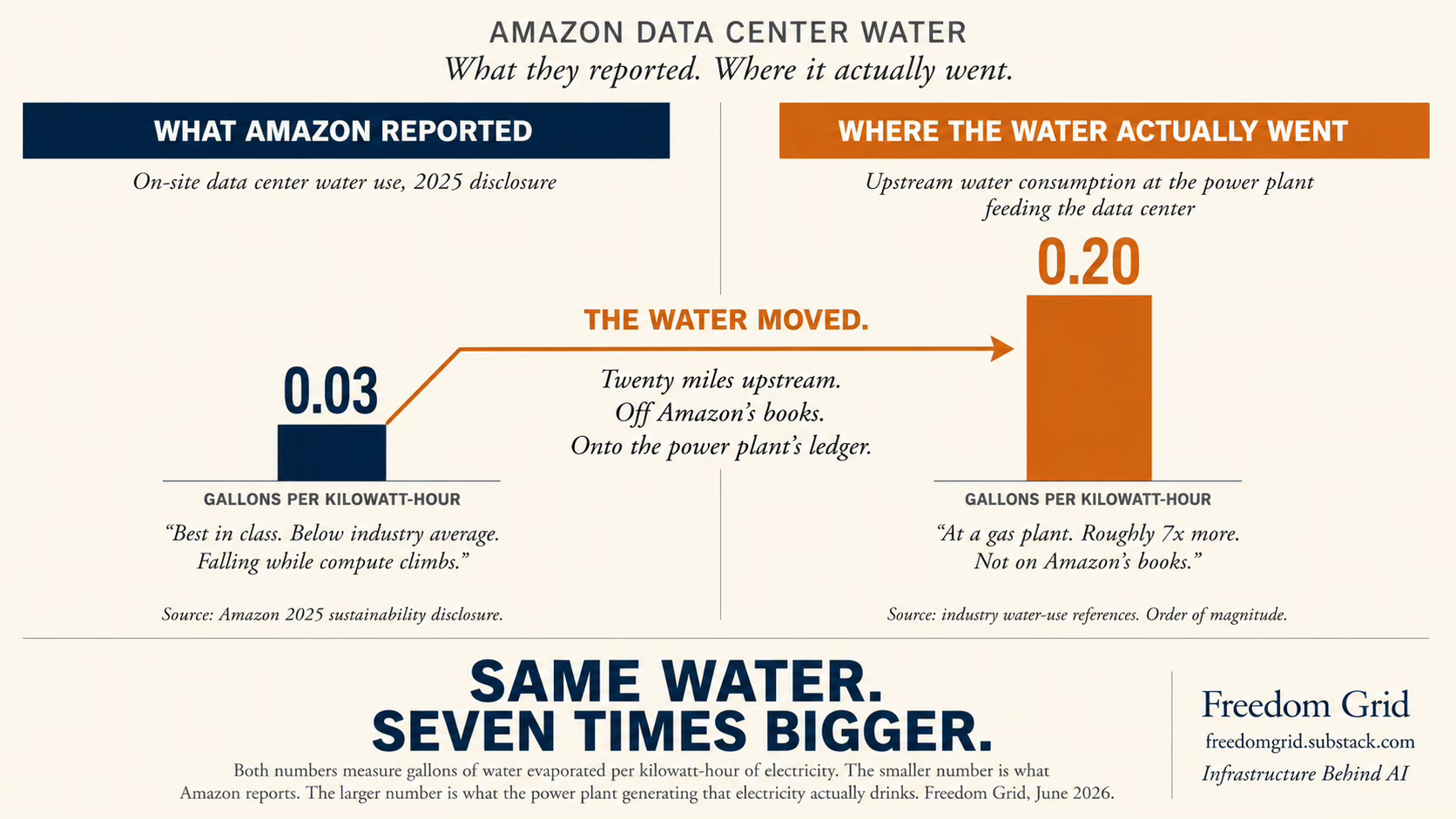

Amazon did something this week it had never done before. It told us how much water its data centers drink: about 2.5 billion gallons worldwide last year. And it wrapped that disclosure in a flex, that it actually cut its total water use in 2025 even while adding data center capacity, down to roughly 0.03 gallons for every unit of electricity it runs. Best in class, well under the industry average, water use falling while compute climbs. A genuinely good number, on its face.

I went and looked at how they pulled it off, and it flipped the whole water question around for me. So let me walk you through what that 0.03 actually means, because the headline number is real and the story it tells is mostly horseshit. Then let me show you where the real water, and the real money, actually sits, because it is not where the crowd is yelling. It is what we own and what we are watching.

The trick, and the catch

Here is how they did it, and it is clever. Amazon runs its buildings hot and cools them with air for most of the year instead of evaporating water on site. They let the halls run warm, up around 85 degrees, and only break out the water-hungry evaporative cooling on the hottest days, less than 10% of the year. Run air instead of water, and your on-site water number falls off a cliff. That is the 0.03.

But moving that much air is not free. Air is a lousy way to move heat compared to water, so air cooling burns a lot more electricity to do the same job. Amazon did not eliminate the water. They converted it into a bigger power bill. And that power gets generated somewhere, by a plant that drinks roughly seven times more water per unit to make the electricity than the data center would have used cooling itself directly. So Amazon took its on-site number down to 0.03 and shoved multiples of that water upstream, onto the power plant’s ledger, off its own books. The water did not go away. It moved, and it got bigger on the way.

Amazon’s own head of energy and water for the Americas basically telegraphed the problem. He said a water-efficiency ratio is “the best metric” and waved off the absolute volumes as “just big numbers.” That is the oldest move in disclosure. Offer the flattering ratio, bury the ugly total. When somebody hands you the per-unit number and tells you not to worry about the big one, look at the big one.

And the air-cooling move has a clock on it anyway. This is a one trick pony that probably ends in 2026. The next generation of AI chips runs hotter and denser than air can handle. That is why liquid cooling is already taking over the high-end builds, and liquid cooling, by definition, puts water back at the chip. The campus number is going back up regardless. The air trick buys a few years and shifts the optics. It does not repeal physics.

We are all looking in the wrong place

Now the part I want to own, because I had it backwards in my own head, and I would rather tell you that than pretend I always saw it. I knew the water was partly upstream, at the power plants instead of the data centers. What I did not understand was the magnitude. It is not a footnote to the data center number. It is the whole damn story.

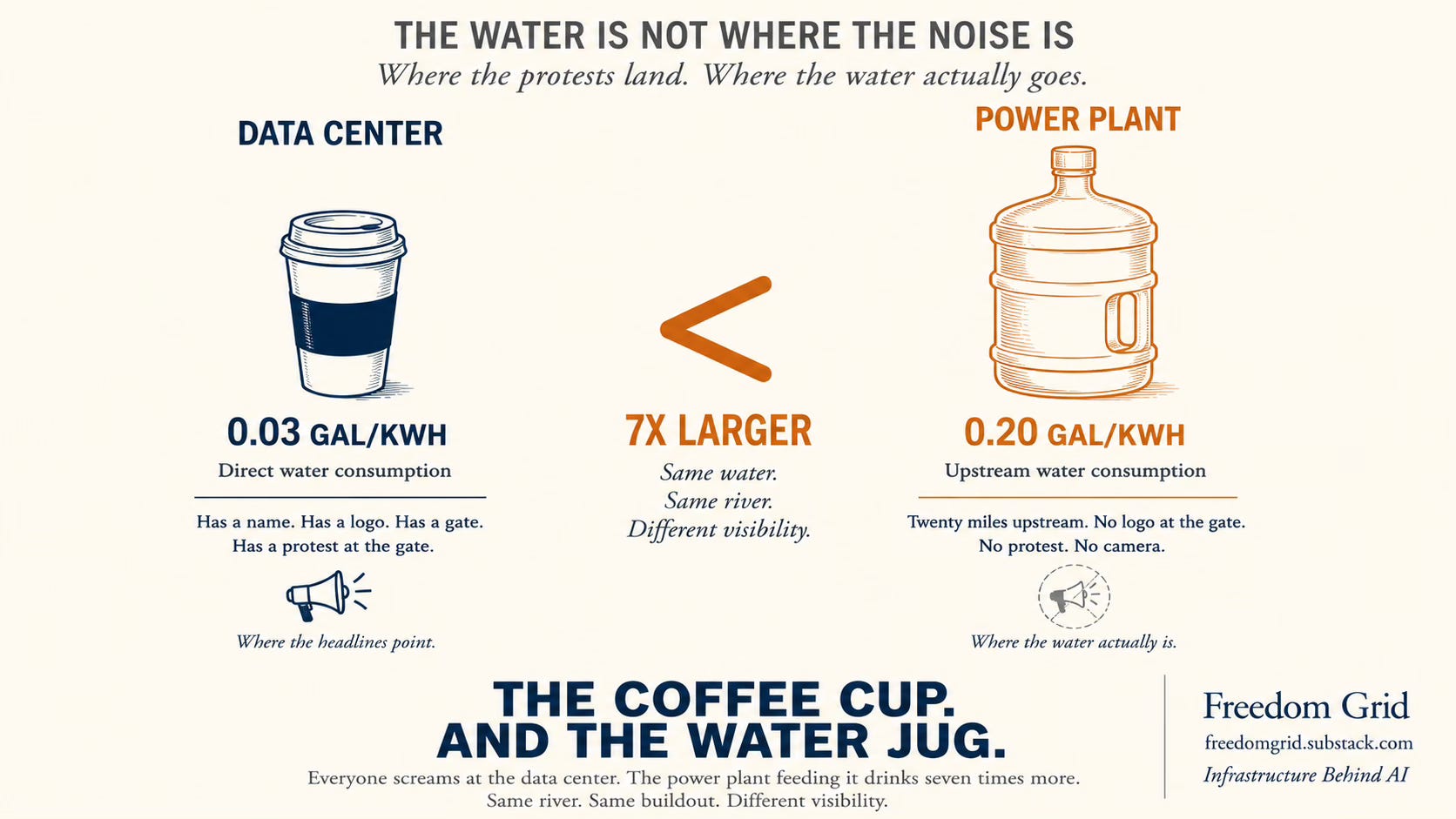

The physics is simple. A combined-cycle gas plant, a coal plant, and a nuclear plant all make electricity the same basic way: boil water into steam, use the steam to spin a turbine, then cool the steam back into water so you can do it again. That last step, condensing the steam, evaporates water, and a lot of it. The numbers, and I will flag these as order-of-magnitude because the ratios are rock solid even if the third decimal is not: a data center runs about 0.03 gallons per unit of power. A gas plant runs about 0.2, roughly seven times more. A nuclear plant runs about 0.67, more than twenty times more. Wind and solar run essentially zero, because there is no steam, nothing to condense, nothing to evaporate. You wash the panels occasionally and that is it.

The power AI actually needs is firm, around-the-clock baseload, and the firm baseload options, gas and nuclear, are exactly the thirsty ones. The dry options, wind and solar, are the intermittent ones that cannot carry a data center by themselves. The constraint and the cleanest solution are fighting over the same molecule.

So why is every protest sign and every zoning fight pointed at the data center? Because the data center is the visible villain. It is the new building in town. It has a name and a logo on the gate. It shows up at the county meeting where people can stand up and point at it. The power plant feeding it is twenty miles away, its water filed under the power sector and smeared across a fleet of old plants nobody has protested in thirty years. The data center is the teaspoon everybody screams about. The power plant is the bucket nobody looks at. Same river, same buildout, same demand. One of them just has a face.

Make no mistake about where the real constraint sits. It sits at the plant, where the volume is multiples higher. But here is the trap in thinking it is only there: the campus number climbs too, as cooling goes liquid. This thing grows big at both ends. The blame is aimed at the small end. The constraint is heaviest at the hidden end. And both ends grow from here.

The honest caveat, kept in front

Here is the caveat I am keeping right out front, because the second you oversell this you lose the plot. The absolute water volume is still small next to agriculture. Americans watering their lawns dwarf every data center and every power plant feeding them, combined. This is not a national water shortage story, and anybody selling it to you as one is selling you fear. McKinsey puts US data centers at well under a tenth of a percent of total US water use today.

So why does it matter at all? Two reasons, and neither one is gallons.

First, it is a concentration story. The water is small nationally but it lands hard in a handful of stressed basins where the campuses and plants actually cluster: Virginia, Texas, Georgia, Arizona. A rounding error nationally can be a genuine fight locally, and local is where permits get approved or killed.

Second, and this is the one that decides where the money goes, it is a spend story. Think about the difference between a gallon of farm water and a gallon of data center water. Farm water is untreated, it runs down an open ditch, and it costs pennies. The water that feeds a data center and the plant behind it gets filtered, chemically treated, run through reverse osmosis, recycled, metered at every step, and in places where you are not allowed to discharge it, boiled down to a solid so there is nothing left to dump. Same molecule, but the dollars per gallon run something like a hundred times higher. And a lot of it has to be built from nothing, because these plants and campuses get sited where the land and the power are, not where the water already is. You are not tapping an existing system. You are building one.

Put rough numbers on it. Direct data center cooling water in the US was around 17 billion gallons in 2023, and it is on track to roughly double by 2028. Stack the upstream power-plant water on top and the new consumptive demand from this buildout runs toward the order of a hundred billion gallons a year by 2030, and I will flag that as a blended estimate, not a precise figure. The piece I care about is the build cost: somewhere in the range of ten to twenty billion dollars a year of new water infrastructure by 2030 that does not exist today. That is not a one-time earnings pop. It is roughly three to seven points added to the annual growth rate of the water-exposed businesses, sustained for a decade. That is the kind of thing that compounds and re-rates a multiple. For the diversified giants it is a grind higher. For the small pure-plays it is a bigger swing off a smaller base. It is slower and steadier than the power trade. It is also load-bearing.

The power plant does not get turned up until the water gets built

This is the part that actually reframes how I am watching the whole buildout. Everybody tracks the gas turbine queues. Everybody tracks transformer lead times running past two years. Those are real constraints and worth watching. But water is the constraint underneath them. A plant can have its turbine slot booked, its transformer ordered, and its grid connection approved, and it still does not run without treated, metered water on site. Same for the campus. Water is a hard gate sitting under all the gates everyone is already counting, and because it is less visible, it is earlier in being priced. That is the whole thing in one sentence. The power does not flow until the water does.

If you want to know whether the smart money has figured this out, watch what it buys, not what it says. In March, Ecolab agreed to buy a company called CoolIT for 4.75 billion dollars in cash, at about 29 times forward earnings. CoolIT makes the liquid-cooling hardware that bolts directly onto the chips. Ecolab is a water-chemistry company. A water company just bought cooling hardware, which means it now owns both halves of the data center heat problem, the chemistry and the metal. You do not pay 29 times forward for a business unless you believe the category is about to re-rate and you cannot afford to be left out. That is the smartest money in industrial dealmaking pricing AI as a water story before retail has finished pricing it as a power story.

And here is the catalyst I am watching for. Right now, almost nobody reports their upstream water, the water their power plants drink on their behalf. Only Meta volunteers it. Everyone else’s real footprint is understated by exactly the amount their generation evaporates. The day a regulator forces companies to disclose that indirect water the way they were eventually forced to disclose indirect carbon, the hidden cost of the grid-powered path lights up on paper, and the low-water, on-site path gets repriced overnight. That is a stroke-of-a-pen event, and it is sitting out there waiting.

What we own

So here is where we actually sit. These are the water and water-adjacent names in the book.

Xylem, ticker XYL, is the straightforward one: pumps, treatment systems, and water meters. The picks and shovels of moving and cleaning water.

Ecolab, ECL, was a water-chemistry name. After the CoolIT deal it is a two-sided water-and-cooling play, sitting on both the chemistry and the hardware of the data center heat problem. That deal moved it from a side holding to something more central.

Watts Water, WTS, makes the valves, flow control, and backflow gear that tie a building into the municipal water main. Unglamorous, necessary, everywhere.

SPXC spans two columns at once. Its Marley business builds the cooling towers where this water actually evaporates, at power plants and data centers both. A cooling name and a water name in the same ticker.

Itron, ITRI, spans the other crossover. We bought it for electric metering and the grid-edge layer, but it also does smart water metering and leak detection, which is the measurement layer this entire fight runs on. You cannot regulate, price, or ration what you cannot measure, and Itron sells the measuring.

For the record, some of what we own is not a water play at all, our gas and EPC infrastructure names, and I am keeping those out of this cut so the water picture stays honest.

The watch list

Now the bench, the names we are watching but do not own yet. I score these on two separate axes, because mixing them up is how people get hurt. The first is our composite score, one number that folds in margin of safety, financing certainty, how cleanly the name fits the build, and our read on what could break it. The second is recognition, which is just how much of the story the market has already priced in. A name can score well and already be expensive. A name can be cheap and still score poorly. Two different questions.

The core water plays here are BMI, VLTO, CNM, MWA, PNR, ERII, and VEOEY. The rest are adjacent infrastructure riding the same buildout.

ERII is the whole lesson in one line. It is the most ignored name on that list and it carries the highest asymmetry, and it still only scores a 5, because asymmetry and quality are not the same thing. The pulled guidance, the margin collapse, and the leadership turnover cap it until the next quarter tells us whether that is a delay or real damage. That 5 is the discipline that keeps me from backing up the truck too early on a cheap, broken-looking name. ERII and MTZ both land at 5 for the exact opposite reasons: MTZ is too expensive, ERII is too uncertain. One number, two completely different problems, and you had better know which one you are holding.

Zoom out

Step back and here is the shape of it. This is a ten to twenty year build of deeply unglamorous plumbing that the entire AI story quietly sits on top of. The gallons stay small against the lawns and the farms, and they always will. The spend does not stay small. It compounds, every year, for a decade, because no plant and no campus runs without the water system underneath it. The gap between how boring this looks and how essential it actually is, that is the whole opportunity.

And I want to be clear about one thing, because it is the opposite of how these pieces usually get sold to you. I am not telling you nobody sees this. The people who know exactly what they are doing see it. Ecolab sees it, it just wrote a 4.75 billion dollar check on it. We positioned into this early and on purpose, because we understood from the start that it is an engineered system, not an irrigation ditch. The crowd is not blind. It is just pointing at the wrong end of the pipe. Do not sleep on water. Look upstream.

Disclosure: I own positions in companies discussed here, including Xylem, Ecolab, Watts Water, SPX Technologies, and Itron. The author may hold positions in companies discussed. This is not investment advice. Do your own work, and size your own risk.